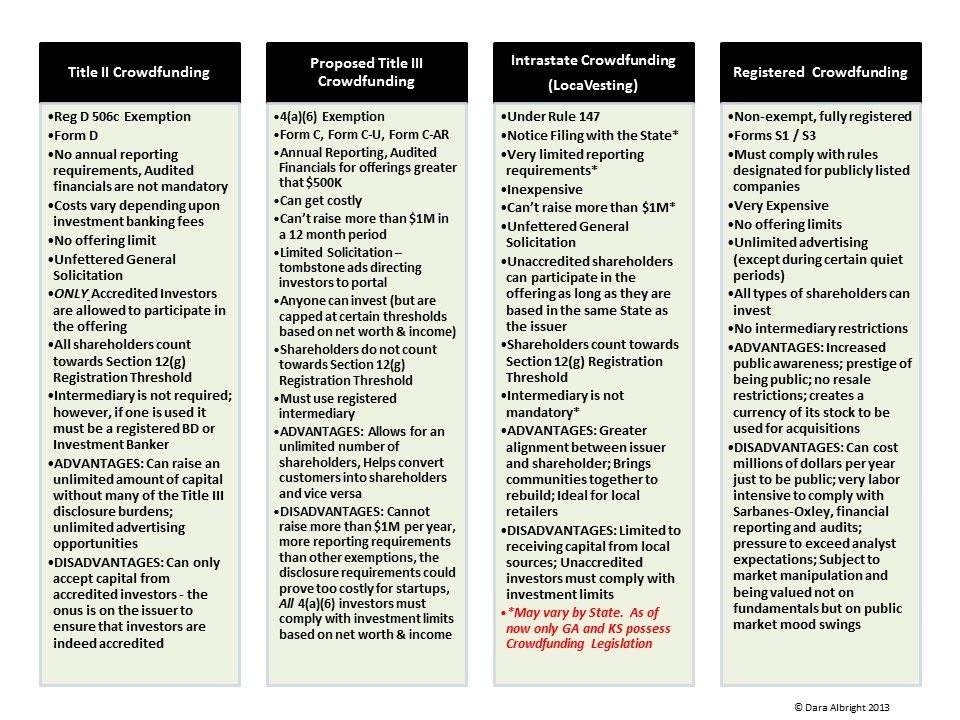

The long awaited Title III Crowdfunding Rules were finally proposed last week by the SEC. Although the 568 page document seems like a mere footnote in comparison to the Obamacare bill, it’s still a lot to digest considering most attention spans these days lack the capability of reading a complete tweet.

In all sincerity, I commend the SEC for putting a great deal of diligence into a legislation that has the potential to reinvent capital formation and democratize the flow of capital. However, after reading the proposed rules (and admittedly falling asleep once or twice), I’m struggling to understand why issuers would opt for this type of financing structure over other more attractive crowdfinance methods.

For instance, why would an issuer raising $1M subject itself to a financial audit, additional form filings and advertising limitations when it can just as easily complete 506c offering where there are no offering limits, no advertising restrictions, no audit requirements and no ongoing filing obligations?

While I remain a staunch supporter of interstate securities crowdfunding, my fear is that Title III crowdfunding (as proposed) will have difficulty finding mainstream adoption. The additional regulatory burdens will make the cost of raising small amounts of capital too high for most emerging businesses. And when capital is too expensive, neither issuers nor shareholders stand to benefit.

That said, Title III crowdfunding might prove best when used in conjunction with other crowdfinance financing techniques. My advice to issuers and bankers would be to get smart on the various corporate crowdfinance options and understand which mechanism best suites specific industry sectors, regions and market capitalizations. My comparison chart below can provide some guidance as it illustrates the benefits and drawbacks of selected crowdfinance offerings including proposed Title III Crowdfunding, 506c offerings, Intrastate Crowdfunding and Registered Crowdfunding.

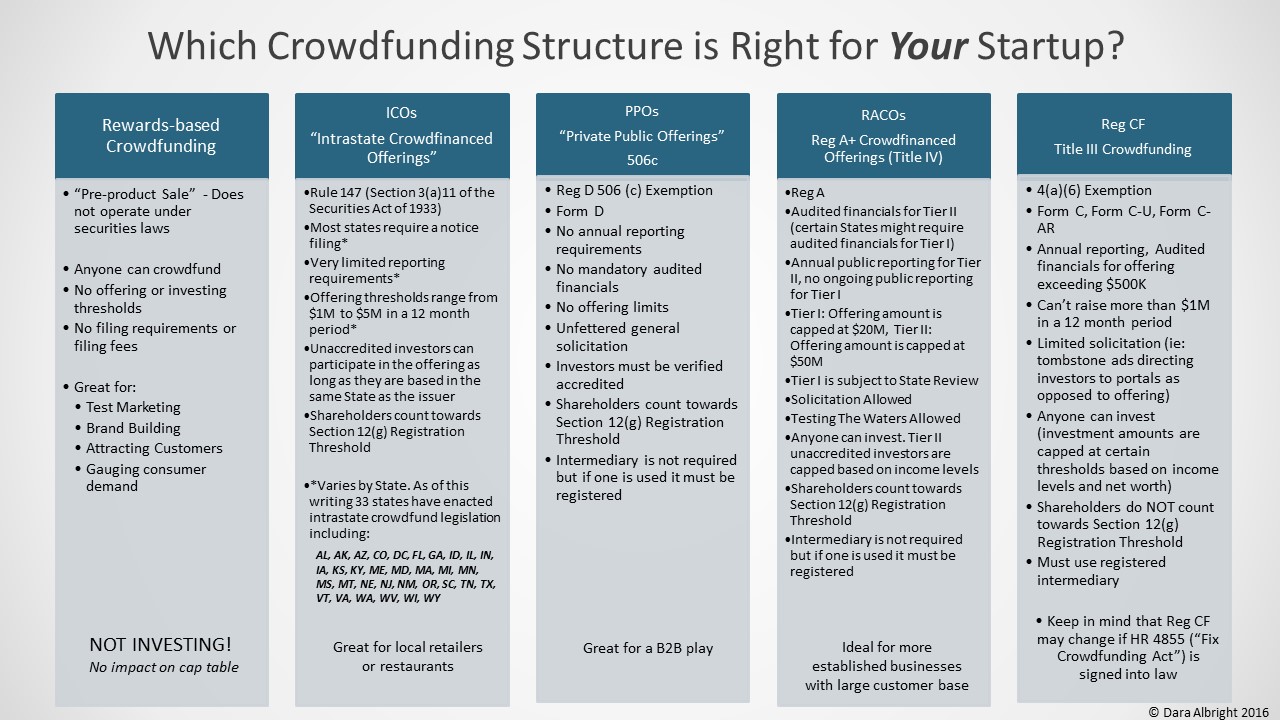

******The above chart is dated. Use the updated chart below for reference:

Leave a Reply